On 12 June 2026, the US Department of Commerce issued an emergency directive that forced Anthropic to suspend foreign nationals from using Claude Fable 5. It came suddenly with no exemption for allied nations and no appeals process. One jurisdiction flipped a switch, and the world’s access to a leading piece of frontier artificial intelligence (AI) went dark.

The ban, which the US has only now begun to lift after weeks of diplomatic fallout, marks more than an AI safety controversy. It crystallises a question that European and UK policymakers have been racing to answer through an unprecedented wave of legislative and industrial interventions. Namely, when a single nation controls the infrastructure upon which your economy, public services and national security depend, what does sovereignty actually mean – and can you build it quickly enough?

This article examines whether Europe and the UK can close a digital sovereignty gap that decades of dependence on American technology have rooted in the continent’s economic foundations. Drawing on economic data, historical precedent and academic analysis, it looks at whether catch-up remains possible and tests that against three prerequisites demonstrated by successful late-developer states in modern history. These are unified strategic funding at a scale that matches the competition, the willingness to use internal markets as an exclusionary weapon, and the humility to copy rather than insist on innovating.

Urgency in Brussels and Westminster

The recent flurry of policy announcements suggests that Brussels and Westminster are gripped by some urgency.

The European Union’s (EU) Cloud and AI Development Act – part of the European Commission’s AI Continent Action Plan – proposes a single EU-wide sovereignty framework with four escalating levels of autonomy, from basic physical data residency (Level 1) through to full software supply chain transparency and demonstrated independence from third-country interference (Level 4). The act also targets a threefold expansion of European datacentre capacity by the 2030s, backed by streamlined permitting and improved access to energy, land and financing.

Alongside this sits the Chips Act 2.0, which shifts the EU’s semiconductor strategy from supply-focused investment to demand cultivation. Its predecessor mobilised more than €52bn in public and private investment and created an estimated 46,000 jobs. The sequel introduces “grand challenges” aimed at industrial development of AI-critical chips, demand accelerators to speed products to market, and state aid provisions for first-of-a-kind fabrication projects not yet present in the Union.

The EU Open Source Strategy completes the triad, mandating public administrations to act as anchor users of open source alternatives – cloud, workplace tools, secure email – and developing a sovereign “Open Internet Stack” designed to displace proprietary foreign software from government workflows.

The UK, operating outside EU mechanisms but facing identical structural vulnerabilities, has assembled its own arsenal. The £1.1bn sovereign compute strategy – announced by technology minister Liz Kendall with the declaration that “AI is the defining currency of economic and hard power in today’s world” – allocates £750m to a national AI supercomputer, including £400m for specialist chip procurement. A £120m AI hardware innovation programme funds domestic chip design and testing. The £500m Sovereign AI Unit, launched in April 2026, aims to become the primary investment hub for high-potential UK AI startups, while a separate £500m sovereign AI fund targets growth-stage companies with investments between £1m and £10m.

The key levers of digital sovereignty

These measures can be grouped into four strategic levers that the EU and UK are pulling simultaneously:

Supply-side industrial policy – the state directly funding physical infrastructure to bypass market reliance on foreign hyperscalers.

Procurement-led sovereignty – using public sector purchasing power to set market standards and force technical requirements on suppliers, from open source mandates to local data residency.

Regulatory shielding – establishing legal frameworks, such as France’s SecNumCloud 3.2 qualification and Germany’s BSI C3A two-tier cloud autonomy criteria, that force foreign providers to meet sovereignty definitions or face exclusion from government workloads.

Innovation ecosystem support – targeted grants and investment funds designed to cultivate homegrown intellectual property.

The cumulative investment is substantial on paper. But it must be measured against a global technology economy in which the imbalance of power is not only large but structural.

Data shows US digital dominance

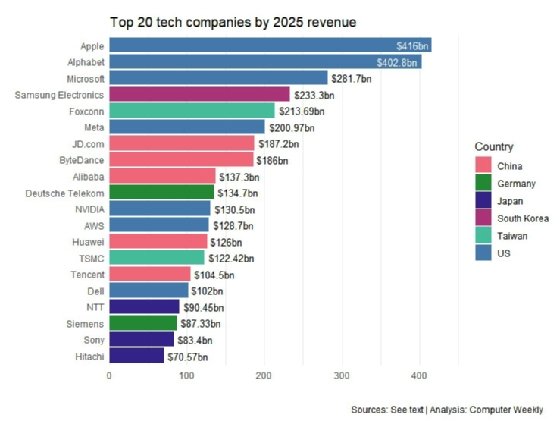

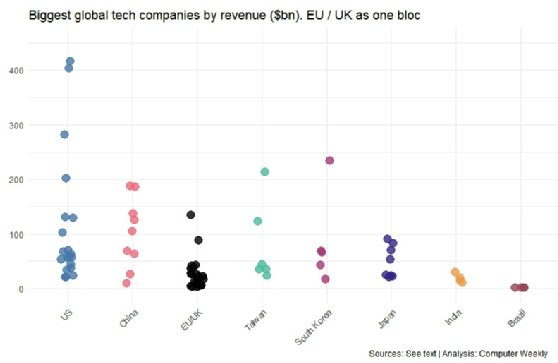

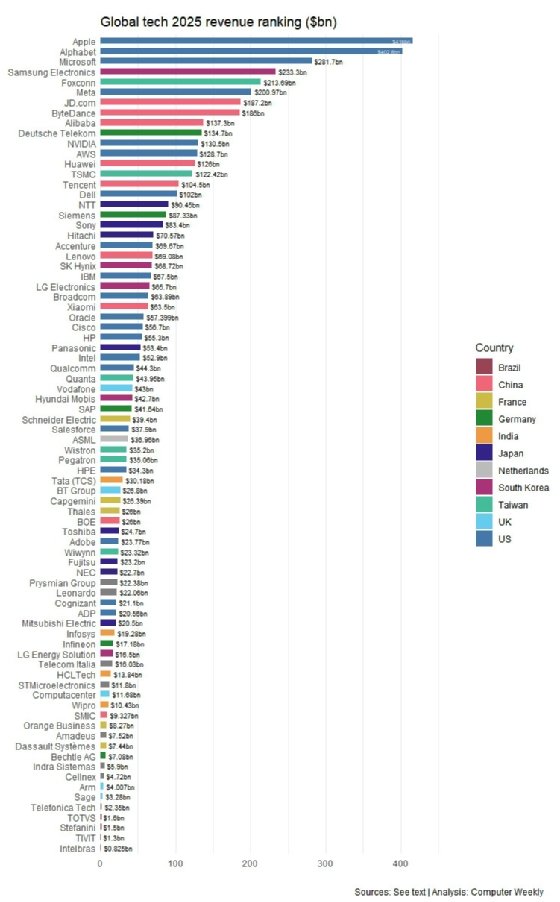

Computer Weekly analysis of audited annual reports and regulatory filings, benchmarked against World Bank and IMF GDP statistics, reveals that US-headquartered technology firms generated combined global revenues exceeding $2tn in their most recent fiscal years.

Microsoft alone posted $281.7bn – more than the combined tech revenue of every major firm headquartered in France, Italy, Spain and the UK, and rivalling Germany’s entire listed tech sector.

Amazon Web Services (AWS) contributed $128.7bn in cloud infrastructure revenue, Alphabet $402.8bn, and Nvidia – the semiconductor designer whose graphics processing units (GPUs) power the AI revolution – $130.5bn.

By contrast, Europe’s largest technology companies operate at a fraction of that scale. Germany’s SAP, the continent’s flagship enterprise software firm, reported $41.6bn. France’s Dassault Systèmes reached $7.4bn. The UK’s ARM – a globally significant semiconductor intellectual property (IP) designer – generated $4bn.

No European-headquartered company operates a hyperscale cloud infrastructure business at a level competitive with AWS, Microsoft Azure or Google Cloud. The delivery model that underpins the modern digital economy – elastic, on-demand compute – is almost entirely American-owned.

Tech GDP as a percentage of national output tells the same story from a different angle.

The US tech sector accounts for 7.1% of GDP against a $30.5tn economy. The UK sits at 5%, Germany at 5.1%, France at 5.2%. The gap appears modest until measured against the countries that have already caught up. South Korea registers 12.3% tech GDP – the highest of any advanced economy – built on Samsung Electronics ($233.3bn), SK Hynix ($68.7bn), and a state apparatus that for decades directed credit to specific firms through state-directed credit mechanisms. Taiwan hits 12% on the back of TSMC ($122.4bn) and Foxconn ($213.7bn), companies incubated under conditions of strategic state protection and explicit government coordination.

The state as driver of development

What distinguishes the South Korean and Taiwanese outcomes from European aspirations is not merely the scale of investment but the political architecture that directed it.

Andrew Wright, a lecturer at Hult International Business School who specialises in international political economy, frames the distinction through the lens of historical catch-up dynamics.

“Germany and America overtook British leadership through protectionism and state promotion of industry,” notes Wright. “As a result, they developed giant monopolistic – or, more accurately, oligopolistic – corporate giants. Scale was important then and still is.”

The post-war generation of East Asian developers – Japan, then Korea, then Taiwan – intensified this model.

“These countries used much more extensive state support, protection, and, frankly, overall direction,” Wright explains. “All of these states borrowed and stole technology, promoted giant firms, protected home markets and largely copied advanced nations while benefiting from lower costs.”

The pattern is so consistent that the economic historian Alexander Gerschenkron identified a typology: the later the catch-up project, the greater the role played by the state. China, the most recent entrant, represents the apotheosis of this trajectory – state capitalism at continental scale, with Alibaba ($137.3bn), Tencent ($104.5bn) and Huawei ($126bn) now rivalling Western incumbents on revenue and increasingly on technological capability.

But the East Asian precedent carries a complicating element for Europe.

Cheap labour – the mechanism that enabled Korea and Taiwan to drive export-led growth while protecting domestic markets – is structurally unavailable to advanced European economies.

“Europe cannot emulate this in competing with the US,” Wright argues. The more relevant parallel lies further back in history. “In the late 19th century, low wages were not a major factor in the rise of the US and Germany. It was more about state tutelage, the growth of the giant corporation, and the systematisation of research and development.”

Responding at scale hampered by fragmentation

This distinction proves critical when evaluating the three prerequisites against Europe’s present position.

The first prerequisite – unified strategic funding at a scale that matches American finance – faces the immediate obstacle of fragmentation. The UK’s £1.1bn sovereign compute programme and the EU’s €52bn Chips Act mobilisation represent genuine political commitment, but they operate through entirely separate governance structures, procurement pipelines and strategic priorities.

South Korea’s window guidance system, by which the central bank literally directed private banks to extend credit to designated firms, required a concentration of financial authority that no European institution – not the European Investment Bank, not the European Central Bank, not any national treasury – currently possesses.

“Only a hugely concentrated strategic mechanism of funding can compete with what the Americans now have available to them,” Wright observes, “partly due to their past and partly due to the sheer size of American finance.” He adds: “Current efforts to seed little developmental pockets, or the shoots of venture capitalism, cannot possibly compete.”

Using the market: The Airbus example

The second prerequisite – the willingness to use Europe’s internal market as an exclusionary weapon – has a proven precedent.

Airbus, the European aerospace consortium, now competes directly with Boeing after decades of state-backed development that American free-market economists once derided as incapable of picking winners.

I would see Airbus as a model. If I was a pro-EU policy maker, I would stop American private companies from feeding off funds and contracts of the European states, and replace those relations with European contractors Andrew Wright, Hult International Business School

“I would see Airbus as a model,” says Wright. The logic transfers directly to digital infrastructure: “If I was a pro-EU policy maker, I would stop American private companies from feeding off funds and contracts of the European states, and replace those relations with European contractors.”

Elements of this approach are already visible. The UK’s Science, Innovation and Technology Committee has proposed a “cloud consumption dashboard” to publicly track contract awards by supplier, mandating SME spending targets and break clauses in contracts with foreign providers. The Procurement Act 2023 is being updated to require public sector bodies to prioritise open source solutions. The EU’s four-level sovereignty framework creates a ratcheting mechanism by which providers must demonstrate progressively deeper independence from third-country jurisdiction to qualify for sensitive workloads.

The counter-current, however, is powerful. Decades of procurement decisions have entrenched American hyperscalers within European public sector architecture.

The network effects are self-reinforcing. The more departments standardise on a single cloud platform, the harder and more expensive exiting becomes.

Wright describes this as “path dependence” – the accumulated weight of past choices that makes deviation costly even when the strategic case for change is overwhelming. “Europe has existed under American tutelage, allowing US firms access and the development of dominance,” he notes. “Breaking out of this is costly and difficult.”

Copy, don’t innovate

The third prerequisite – the willingness to copy rather than insist on innovating – cuts against Europe’s self-conception as a centre of original research.

Wright points to a historical irony. “Much of the technology that has fed the American machine was originally developed in Europe. Yet Europe has often been unable to control and commodify it, or build the giant dominant firms that emerged from it,” he says.

The East Asian developers faced no such cultural constraint. “They rarely innovated; they mostly copied,” says Wright.

The EU Open Source Strategy represents an implicit acknowledgement of this logic – building a catalogue of open alternatives that, by definition, replicate proprietary functionality rather than inventing from scratch. The Gaia-X federated infrastructure initiative creates interoperability standards designed to let local European providers link services in direct competition with non-EU hyperscalers, again a copying-and-competing model rather than a leapfrogging one.

Whether European political culture can sustain this pragmatic posture – building what works rather than what is original – remains an open question.

Digital sovereignty at a crossroads

The question that faces European policymakers is not whether digital sovereignty is desirable but whether the window for achieving it remains open.

The Fable 5 episode demonstrates that dependency is not a theoretical risk that can be managed through contractual fine print. It is an operational reality that can be triggered by a foreign government’s unilateral decision, with consequences that cascade through every service, every department, and every citizen who relies on infrastructure they do not control.

The revenue data suggests the structural gap is widening, not closing. American technology firms grow at rates European competitors cannot match, fuelled by a venture capital ecosystem, a stock market depth and a military-industrial procurement pipeline that Europe has no equivalent of.

The US, Wright argues, operates a “hidden developmental state” – less visibly directive than the East Asian model but no less effective, leveraging defence spending, public sector contracts and deep state-corporate integration to sustain technological dominance while maintaining the rhetorical posture of free enterprise.

The conditional verdict, then, is that Europe and the UK can catch up – but the path demands a level of political coordination, financial concentration and strategic pragmatism that the continent has rarely mustered outside of wartime mobilisation or the Airbus project.

The measures now being deployed are genuine in intent and substantial in scale by historical European standards. Whether they are sufficient in speed and coordination to overcome decades of accumulated dependency is the question on which the next decade of European digital sovereignty will turn.

{kind=link}